Opinion

As house prices surpass 2007 levels in Spain, is there a danger of another housing bubble?

Andalusia’s housing market has hit something of a milestone. After 17 years, housing prices have returned to the levels reached in 2007, just prior to the terrible collapse that led to almost a decade of decline. Does this mean we are in another housing bubble that will end in tears, like the last one? Or have we simply finally and fully recovered from the housing collapse but on a more stable, solid foundation?

The price rises continue a trend since the end of the pandemic of increases in both sales and price rises. However, these both have been moderating after the explosion of pent-up demand that followed the pandemic during 2021-22.

A report by Caixa Bank states that prices are expected to rise on average 5% in 2024, though this will fall to 2.8% in 2025. That puts price hikes slightly above inflation but, as Caixa notes, and I have argued, this is primarily the result of a lack of new housing construction.

« 330,000 net households are expected to be created each year in the period 2024-2028, compared to previous projections of around 220,000 households in the same period. In the absence of a significant increase in the housing supply in the coming years, the gap between supply and demand will steadily widen, and this could apply further pressure on home prices, especially in areas that are experiencing more rapid demographic growth. »

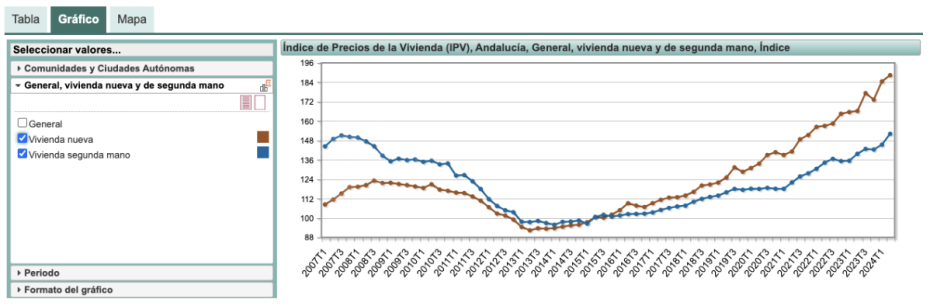

There are several things that must be said about house prices surpassing those of 2007. The first thing to note is that the price of new houses in Andalusia surpassed the peak price back in 2019 – it has continued climbing since. The other notable feature in the statistics from the National Institute of Statistics (INE) is that new houses suffered less of a price collapse and a sharper recovery once the housing market picked up after 2015.

Second-hand homes, on the other hand, suffered a much steeper price collapse and have had a slower recovery since 2016. I have discussed this on previous occasions and looked in detail at the fact that Spain is not building enough houses to meet the growth in the number of households. The unequal price growth you see in the INE graph reflects that, which reinforces what Caixa writes in their research paper, quoted above.

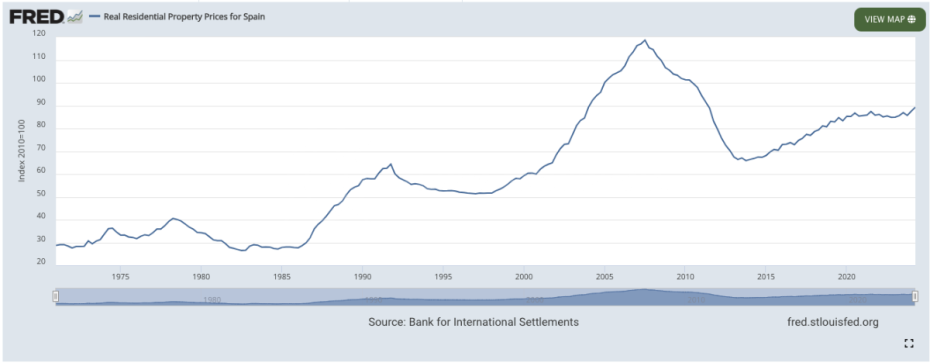

If we take another step back and look at longer term trends in Spanish housing prices, we also get a better sense of the bigger trends that have unfolded. Prior to 1986, housing prices in Spain were quite stable, as the following graph from the US Federal Reserve shows. But in 1986 Spain (and Portugal) joined what is now the EU. From that moment until 1991 – when there was a global recession – Spain had its largest ever run up in prices.

In the 1990s there was a recession, caused in part by high-interest rate policies and austerity, to bring down public debt. The peseta was also devalued twice, adding further to economic difficulties. But at the end of the decade, interest rates declined, and Spain entered the Eurozone. This lowered interest rates further and provided more growth, investment, and access to credit.

While Spain had its specific features, like joining the Euro, it was part of a general trend of financial liberalization. Especially after the dot-com bubble burst in 2000, there was a further, aggressive round of lowering interest rates and getting credit was made easier internationally.

This was done to reduce the intensity of the recession, with some success. But it also led to a massive run-up in speculation as money became cheap. We now know – and can see very clearly in the Federal Reserve chart – what the ultimate effect of that was, a massive bubble.

At the time, for many people, construction companies and real estate investors, it seemed like a massive opportunity. A lot of people made a lot of money. Many ordinary people bought houses larger than what they could afford. Or they bought second and even third houses that they intended to « flip » for constantly rising prices.

One expression of what we might call that « irrational exuberance » was that people took out variable rate mortgages. Everyone thought interest rates would forever stay low and, anyway, many investors were just going to buy a house and then sell it at a higher price a short time later. It was like free money falling from the sky.

Except that it wasn’t.

The collapse that followed, along with a leap in interest rates to 6.8% by 2010, was incredibly painful for millions of people and for the economy as the crisis spread outwards. However, looking at the Fed chart what is interesting is that the current trajectory of price rises conforms to a normal trendline going back to 1986. It is the bulges the led to corrections that are out of line. That is one piece of evidence that suggests we are on a healthy round of price growth.

Mortgages, debt, and interest

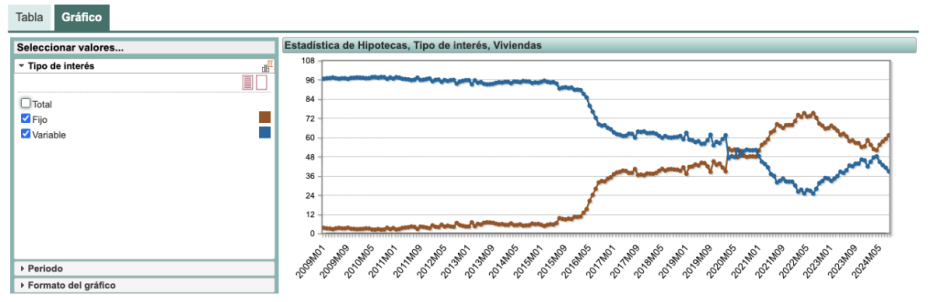

One of the big changes that took place between those peak prices of 2007 and the current housing market is the massive change in mortgage practices. The first thing is that the number of people who took out mortgages in Spain collapsed and has never recovered to pre-2007 levels. During 2006, at the peak, 1.3 million mortgages were taken out in Spain. At the base of the trough in 2013, that number had fallen to about 200,000. In 2023, the number of mortgages taken out in Spain, for the purposes of buying a house was still only 380,000 – just over a quarter the level of the peak.

What’s more, the character of those mortgages has changed dramatically. In 2009, almost all mortgages in Spain were variable rate mortgages – 96%. When rates rose between 2010-12, all those people with variable rate mortages were hit very hard, collapsing the housing market to its lowest point by 2013.

As conditions permitted, including a slowly recovering economy, banking reforms and a push to encourage people back into the mortgage market with more stable, fixed rate mortgages increased in popularity. This was helped by historically low interest rates. The ECB lending rate in 2015 was basically zero. Spain had mortgage rates of 2.12%, which were the cheapest in the EU. This made fixed rate mortgages very cheap and attractive – especially as there was a brief spike in interest rates in 2016 just as the housing market was recovering.

As people moved back into the housing market – if they sought a mortgage at all – it was increasingly likely to be a fixed rate mortgage. Fixed rate mortgages now make up over 60% of all mortgages, as shown by the chart from the INE below. That means that people have locked in their interest rate for the entire duration of their mortgage.

That can reduce the « velocity » of turnover in the market when interest rates go up – as people want to hold onto their cheap mortgages. But it also means people don’t experience a sudden increase in house payments, leading to defaults, which can turn a market correction into a market collapse.

This shift away from mortgages was also part of a more general de-leveraging within the Spanish economy. People spent literally a decade or more clearing up their balance sheets and eliminating debt.

In 2010, household debt in Spain was the highest in the EU-28 at 84% of GDP. By 2023, that debt load had been cut almost in half to 51.1% of GDP. In other words, the current boom in house sales and house prices is occurring simultaneous with Spaniards reducing their debt loads, rather than increasing them, as happened in the lead up to the 2008-2015 crash.

Economic Underpinnings

The overall picture, before even looking at the broader economy, is that the Spanish housing sector is less overpriced, less leveraged with debt and more stable than 2007. The rising prices we see, according to a study by BBVA, are largely driven by an imbalance between supply and demand, rather than speculation and unsustainable froth.

Those imbalances pose real challenges, especially as the formation of new households continues to outstrip the construction of new housing. However, that’s a very different set of problems than Spain suffered in 2007. It remains to be seen how far the demand supply imbalance will continue to push further price increases, especially in the luxury prime sector.

The housing market has a further underpinning, which is a strong Spanish economy. Its strength has been noted by every major institution, from the OECD, to the EU, to the Spanish government itself and to Caixa Bank in a recent report. As the government wrote at the end of September:

« The Executive’s new forecasts raise the growth forecast for 2024 by 3 tenths to 2.7%. In 2025 and 2026, the economy will grow 2.4% and 2.2%, respectively, 2 tenths more than the Government’s estimates so far. »

Caixa Bank basically agrees with these number, as does the EU, but adds that core inflation in the economy is also dropping more than expected. Other statistics show that employment has grown as has Spanish household savings which, at 13.4%, puts it higher than 2008 by 1.4%.

There was a brief dip after the end of the pandemic, when people began shopping again but it has begun climbing again quite rapidly. This is both good and bad. On the one hand, it means that Spaniards are more liquid and less likely to suffer difficulties. On the other hand, it suggests that people are holding back from consumption, which can have an impact on economic growth.

Thus, the overall picture is nowhere near that of 2007 just prior to the bubble bursting. That isn’t to say that there aren’t problems that require attention – like the lack of new house construction to meet demand. But the overall picture in Spain is one of economic health and solid fundamentals, more so than most of Europe. Growth in the EU as a whole will average half the rate of Spain this year.

With all that in mind, I fully expect there to continue to be price growth and a strong housing sector over the next couple of years, barring some major event – like Covid, a Tariff War or worse.

Par Adam Neale | Opinion | 20 novembre 2024